The 2017–2018 Initial Coin Offering (ICO) craze was characterized by high-risk investment, rapid fundraising, and, ultimately, mass fraud. Few cases demonstrate the deliberate conflation of financial hype and technical deception quite like AriseBank. Touting itself as a revolutionary “decentralized bank,” the Dallas-based venture, led by CEO Jared Rice Sr., managed to convince hundreds of investors that they were participating in banking history.

This forensic analysis pulls back the curtain on AriseBank, revealing how its founders constructed a sophisticated fiction of regulatory compliance and technological genius that masked an alleged personal spending spree and resulted in multi-million dollar fraud, swift regulatory intervention, and serious criminal convictions for its executive.

Forensic Overview: The Myth of the $600 Million ICO

AriseBank’s core offering was its proprietary token, AriseCoin, sold through an ICO. The project claimed monumental success almost immediately, creating an illusion of financial inevitability that drew in retail investors.

The Key Financial Claims and Realities:

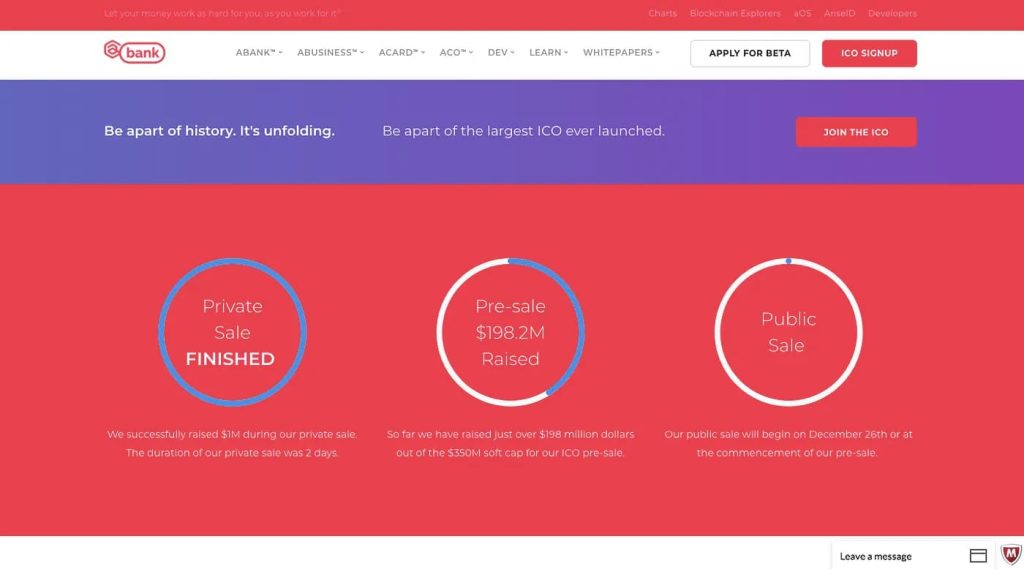

- Claimed Funds Raised: AriseBank repeatedly claimed to have raised an astonishing $600 million of its $1 billion target in just two months.

- Actual Fraudulent Proceeds: The criminal charges against CEO Jared Rice Sr. centered on the successful defrauding of hundreds of investors of over $4 million. Hundreds of investors bought approximately $4.25 million in AriseCoin using cryptocurrencies like Bitcoin, Ethereum, and Litecoin, as well as fiat currency.

- The Discrepancy: The sources note the “most shocking aspect” concerned the total dollar amount raised: while the charges focused on $4 million in fraud, the company had claimed to raise $600 million in a matter of weeks. Prosecutors later deemed the $600 million claim fraudulent.

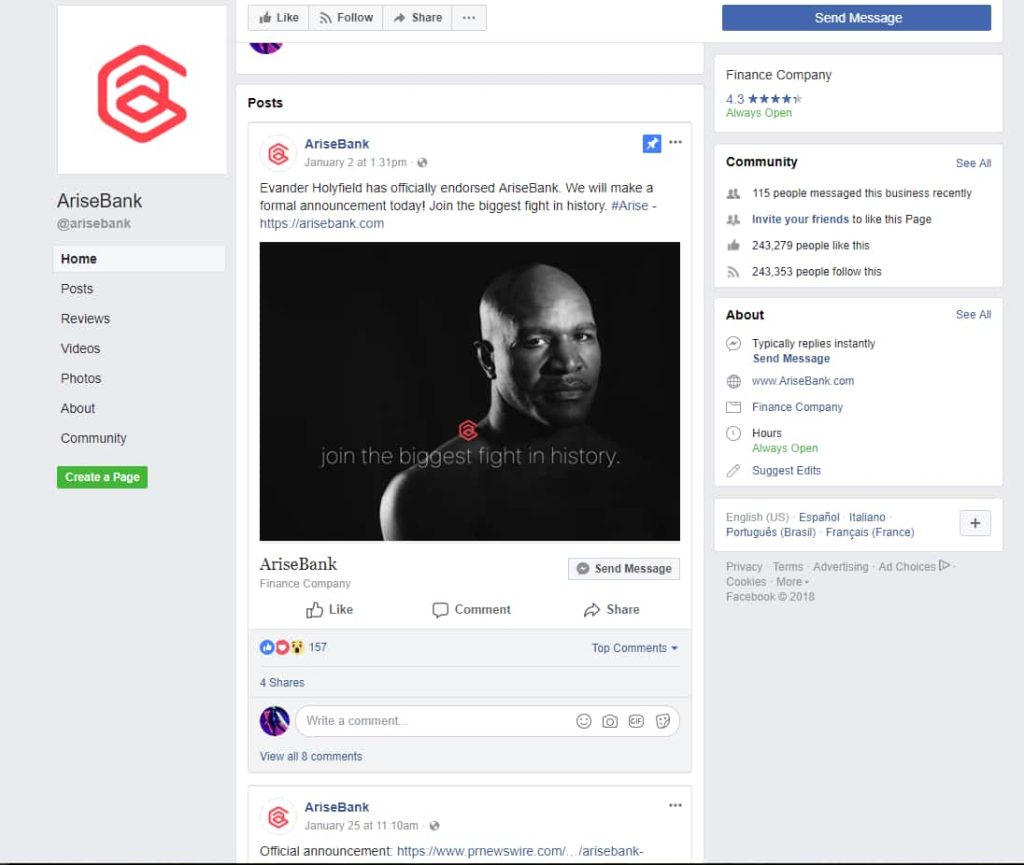

The speed and scale of the purported fundraising—even if largely fabricated—were highly effective “wide dissemination tactics” used alongside social media and celebrity endorsements to lure prospective investors.

Dissecting the Deep Fraud Mechanism: The Illusion of Technical and Financial Legitimacy

The forensic heart of the AriseBank scam lay in its ability to marry the opaque, futuristic promise of blockchain technology with the solid, regulated assurance of traditional banking—all through a web of outright fabrication.

The CEO, Jared Rice Sr., marketed AriseBank as the “world’s first decentralized banking platform”. This platform was said to offer services using over 700 different virtual currencies. The claims hinged on three pillars of supposed trustworthiness, all of which were false:

1. Fictional Regulatory Compliance

In one of the most damning aspects of the scheme, AriseBank repeatedly claimed to offer services that required federal authorization and insurance that it simply did not possess.

“Rice allegedly lied to his investors during AriseBank’s Initial Coin Offering (ICO). Rice told prospective investors that Texas-based AriseBank was the world’s ‘first decentralized banking platform’ which could offer consumers FDIC-insured bank accounts.”

- No FDIC Insurance: The platform was not FDIC-insured.

- No Banking Authorization: AriseBank had never received authorization to perform any banking activity in Texas.

- Fake Partnerships: Rice falsely claimed the platform provided traditional banking services, including Visa credit and debit cards. The investigation confirmed AriseBank never had a partnership with Visa or any other payment card business.

To further cement this false legitimacy, AriseBank issued a press release claiming to have acquired KFMC Bank Holding Company (a supposed 100-year-old commercial bank) and TPMG (an investment banking and management firm). Regulators found that neither AriseBank nor KFMC appeared to be registered with the Texas Secretary of State or the FDIC, and TPMG did not appear to exist.

2. The Contradictory Technology Stack

AriseBank’s technical promises were a catalogue of contradictions and impractical features designed to overwhelm due diligence with buzzwords. The sales pitch claimed the company developed an algorithmic trading application that automatically generated gains by predicting future movements across 700 different cryptocurrencies.

An analysis in the sources questioned the fundamental viability of these claims:

- Impossible Exchange: AriseBank promised an exchange for 700 cryptocurrencies with “several hundred-tausend of trading pairs” and without fees. This promise flew in the face of market realities, where functioning exchanges struggle to ensure liquidity even for a handful of currencies.

- Conflicting Blockchain Foundations: The company claimed its new blockchain was based on multiple, seemingly incompatible technologies, including #rise, #ARK, and #Lisk.

- Blockchain Mobile Phone: The claims extended to developing a mobile phone for around $100 based on a blockchain operating system, a concept deemed far beyond comprehension, given that blockchain systems are typically “pretty slow”.

These highly technical, yet fundamentally unworkable, promises created a facade of complexity—a typical hallmark of schemes that use technical jargon to mask non-existent products.

3. Misappropriation of Investor Funds

While Rice touted “nonexistent benefits in press releases and online”, he was “quietly converting investor funds for his own personal use”. Instead of building the purported decentralized banking platform, the CEO allegedly spent investor money on a luxury lifestyle.

The expenditures listed in court documents included:

- Hotels.

- Food and clothing.

- A family law attorney and a guardian ad litem (an appointed court figure determining a child’s best interests).

Red Flags Ignored: A Case Study in Due Diligence Failure

For prospective investors, AriseBank displayed numerous glaring red flags, which experts urged the cryptocurrency community to heed.

1. Failure to Disclose Criminal History

A massive red flag was Jared Rice Sr.’s documented criminal past, which he allegedly failed to disclose during the ICO. Prior to the AriseBank ICO, Rice had pleaded guilty to state felony charges connected to a previous internet-related business scheme.

The SEC complaint further revealed that Rice was on probation stemming from a 2015 Collin County, Texas, indictment for felony theft and tampering with government records, and also faced a felony indictment in Dallas County for assault. The concealment of this history was critical to the fraud mechanism.

2. Questionable Corporate Transparency and Partnerships

Critical scrutiny revealed significant issues regarding the company’s registration and claimed affiliations:

- Malleable Registration: A financial adviser noted that the website incorrectly listed the company designation as “Arisebank, Gmhb” and later changed the disclaimer, avoiding legal designation entirely. When confronted, Rice claimed it was the “old version,” but failed to provide documentation for its supposed new registration in the US.

- Fake Endorsements: AriseBank leveraged celebrity endorsements and claimed “strategic partnerships,” such as with Bitshares. However, members of the Bitshares community warned investors that the partnership was a scam. Attempts to raise critical questions about AriseBank within related crypto channels were allegedly silenced, with critics being thrown out and negative comments being deleted.

3. Regulatory Warnings Preceding the Halt

Before the federal actions, state regulators had already flagged AriseBank’s activities. The Texas Department of Banking issued a cease-and-desist order in early January 2018, concluding that AriseBank had falsely implied it offered banking business in the state. The SEC complaint followed shortly thereafter, halting the alleged scam.

The Legal Aftermath: Criminal Prosecution and Regulatory Crackdown

The demise of AriseBank was swift, highlighting the increasing vigilance of US regulators toward the burgeoning cryptocurrency market.

Federal Intervention and Criminal Conviction

On November 28, 2018, the United States Department of Justice announced Rice was indicted on three counts of securities fraud and three counts of wire fraud. Jared Rice Sr. was arrested by the FBI in connection with the alleged scheme.

If convicted on all original counts, Rice faced a potential sentence of up to 120 years in federal prison.

Ultimately, Rice, 33, pleaded guilty to one count of securities fraud in March 2019. On August 25, 2021, U.S. District Judge Ed Kinkeade sentenced him to five years in federal prison. He was also ordered to pay $4,258,073 in restitution.

SEC Civil Enforcement and Penalties

The US Securities and Exchange Commission (SEC) launched parallel enforcement actions against AriseBank and its co-founders, Rice and Stanley Ford, for offering and selling unregistered investments (AriseCoin).

The SEC obtained an emergency court order to halt the ICO and freeze assets in January 2018. Notably, this was the first time the SEC had sought the appointment of a receiver in connection with an ICO fraud. The court-appointed receiver immediately secured various cryptocurrencies held by AriseBank, including Bitcoin, Litecoin, Bitshares, Dogecoin, and BitUSD.

In December 2018, Rice and Ford settled the SEC’s charges, agreeing to be held jointly and severally liable for over $2.5 million in disgorgement, prejudgment interest, and civil penalties. They also consented to lifetime bars from serving as officers and directors of public companies and participating in future digital securities offerings.

The AriseBank case served as a stark warning and demonstrated the SEC’s commitment to regulating the sector. The increased enforcement across the cryptocurrency community, including actions by state regulators like Colorado’s ICO Task Force, pushed the industry away from traditional ICOs and toward more compliant Security Token Offerings (STOs).

Writer’s Commentary

The core psychological and technical cause of AriseBank’s success was the weaponization of complexity and speed during an investment bubble. Psychologically, Jared Rice Sr. exploited the pervasive Fear Of Missing Out (FOMO) and the investor desire for a “paradigm shift” by promising revolutionary decentralization alongside guaranteed, traditional safety (FDIC insurance and Visa cards). This fusion—promising the wild gains of crypto while delivering the security of legacy finance—was a highly effective, albeit fraudulent, market differentiator. Technically, the dense, impossible nature of AriseBank’s product claims—a blockchain OS phone, a zero-fee exchange for 700 currencies, a magic algorithmic trading bot—functioned as a sophisticated obfuscation layer. In the heady rush of 2018, many retail investors lacked the technical expertise or the time to question complex, jargon-heavy whitepapers, defaulting instead to trusting the hype of the claimed $600 million raise, celebrity endorsements, and the false promise of regulatory approval. The scam succeeded not just because Rice lied about the money, but because he expertly leveraged technological illiteracy to make the impossible sound inevitable.

REFERENCES

- justice – Cryptocurrency CEO Sentenced to Five Years in $4 Million Crypto Scheme

- tokenist – AriseBank CEO Charged with Defrauding Investors of $4 Million, Faces up to 120 Years in Prison

- businessinsider – The SEC has shut down another ICO — this time an alleged $600 million scam in Texas

- cnbc – SEC halts one of the largest ‘ICOs’ ever as it wades deeper into the murky world of cryptocurrency offerings